IGA Capital Global Macro Update

- Joshua Hawley

- 2 days ago

- 4 min read

'Bonds over Baghdad (Dubai) In-slum-national, underground, the yields pound when the Fed stomps the ground. Like a million elephants or silverback orangutans, you can't stop this inflation train. Who wants some? Don't come unprepared; the market’s here, but when it leaves there, volatility will be a household name.

Weatherman tellin’ us it ain’t gon’ rain rate cuts, so now we’re sittin’ in the DIFC, soakin’ wet in a silk suit tryin’ not to sweat the WTI climb. Hittin’ somersaults without the net as crude clears $100, but this’ll be the year the GCC won't forget.

Don't pull the treasury out unless you plan to bang: Bonds Over Baghdad! Ha, yeah! Don’t even trade unless you plan to hedge somethin’.

May 4th, 2026

Dubai, UAE

Economy:

Equities extended their record-breaking run last week as the S&P 500 notched another fresh record high, capping a 10% surge in April that marked the index’s best monthly performance since 2020. Investors faced a blockbuster week with 44% of the S&P 500 market cap reporting earnings including five of the Mag-7, while central bank meetings from every G7 country took place concurrently. Q1 data showed US growth accelerated amid an AI-driven upswing in business investment, with the artificial intelligence engine powering the economy through headwinds from war-fueled inflation as consumers continued to spend. Tech heavyweights delivered mixed results with Google showing clear payoffs from AI spending while Meta lagged behind, though traders continued chasing semiconductors with such intensity that the SOX Index hit its most overbought level in 15 years, demonstrating markets remain largely unfazed by oil increases as the AI narrative takes precedence.

The Federal Reserve delivered a hawkish pause in what was Jerome Powell’s last meeting as Fed Chair, with stocks dropping and Treasuries selling off in the aftermath as traders digested three hawkish dissents and rate cut hopes for this year were obliterated. Economic resilience reasserted itself heading into the weekend as March PCE data came in line with expectations at 0.7% headline and 0.3% core, while initial jobless claims fell to the lowest since 1969. The combination of surging oil and a divided Fed led investors to price out rate cuts almost entirely, with futures showing increased odds of a hike in early 2027. Although the market appears risk-on from the surface level, under the hood, investors remain uneasy about the macro backdrop with the Iran war entering its third month, oil prices elevated, and a transition to a new Federal Reserve chair now imminent. Equities are caught between escalating Middle East tensions and strong fundamental earnings data, with WTI crude continuing its climb north of $100/bbl., likely marking a turning point for equity markets that would require a tangible peace deal to sustain further upside.

Earnings Calendar:

This Week –

Monday 5/4: Factory Orders; Durable Goods

Tuesday 5/5: Trade Balance; S&P Global US Services PMI; ISM Services; New Home Sales; JOLTS

Wednesday 5/6: ADP Employment Change; U.S. Treasury Quarterly Refunding Announcement

Thursday 5/7: Jobless Claims; Construction Spending

Friday 5/8: Nonfarm Payrolls; U. of Mich. Sentiment; Wholesale Inventories

Next Week – Existing Home Sales; NFIB Small Business Optimism; CPI (Apr.); 10yr U.S. Treasury Auction; PPI (Apr.); Jobless Claims; Retail Sales; Empire Manufacturing; Industrial Production.

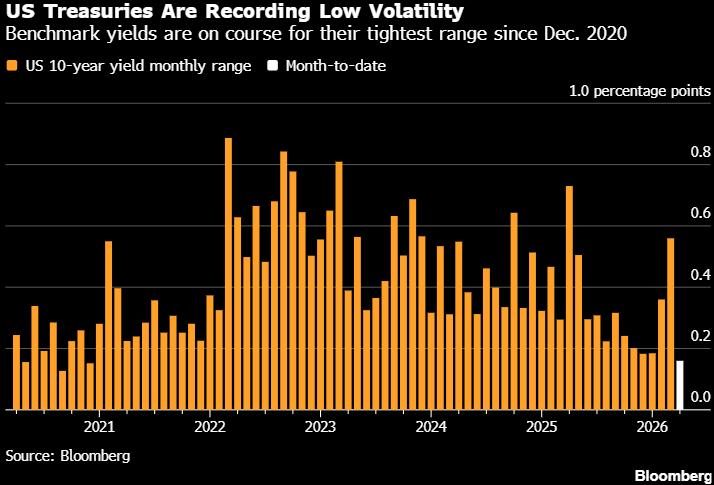

Treasury Yields:

Treasuries posted sharp losses last week as the oil price surge unleashed by the Iran conflict continued to weigh on bonds globally, driving up inflation expectations while pushing central bank policymakers further away from the rate cuts traders had fully priced in before the war began. The 10-year yield climbed as high as 4.42% midweek following a hawkish Federal Reserve decision and President Trump's order to extend the blockade of Iran, with Brent crude surging near $115/bbl., the highest since June 2022.

The yields on the policy-sensitive 2-year note jumped 11bps Wednesday to 3.95%, marking the biggest increase on a Fed decision day since January 2022—just before the central bank started its last hiking cycle—as investors shifted from expecting rate cuts to pricing in the possibility of hikes in 2027. The selloff pushed yields higher across maturities by four to ten bps Wednesday alone, with short-dated tenors most sensitive to Fed rate changes leading the move as three officials dissented against the statement's dovish language. BlackRock Investment Institute noted that the war and elevated inflation will keep government bond yields higher for longer, with strategists warning that a move up to 4.5% in 10-year yields seems more likely than a move down to 4% as sticky inflation and fiscal concerns continue to weigh on Treasuries.

Federal Reserve:

As widely expected, Federal Reserve officials held interest rates unchanged in the 3.50-3.75% range on Wednesday, but the decision exposed the deepest divisions among policymakers since 1992 as four officials dissented from the vote in an 8-4 split. Three regional Fed Presidents, Hammack (Cleveland), Kashkari (Minneapolis), and Logan (Dallas), supported holding rates steady but objected to language in the post-meeting statement suggesting the central bank would eventually resume cutting rates. Meanwhile, Stephen Miran dissented in favor of a quarter-point cut. The statement retained its easing bias despite the unprecedented pushback, highlighting that the war in the Middle East has brought risk to both sides of the central bank's mandate as oil prices remain elevated and inflation concerns mount.

In what will be his last press conference as Fed chair, Jerome Powell announced he intends to remain on the Fed board after his chairmanship ends May 15, citing "unprecedented" legal attacks by the Trump administration that he warned are putting the central bank's independence at risk. Kevin Warsh won backing from the Senate Banking Committee on a 13-11 party-line vote midweek, putting him on track for confirmation as the new chair. Warsh will inherit a committee deeply fractured over the inflation outlook and increasingly resistant to resuming rate cuts despite White House pressure for monetary easing.

FOMC Meeting – Implied Fed Funds Rate:

Implied Overnight Rate: 3.641%

Next FOMC Meeting / Mid-Year Meeting 2026 (June 17th): 3.612%

Last Meeting of 2026 (December 9th): 3.628%

Mid-Year Meeting 2027 (June 9th): 3.682%

If you have any questions or would like to discuss a funding request, please reach out to me using the contact information below.

IGA Capital

Joshua Hawley

+971 50 764 0788

Comments