IGA Capital Weekly Economic Update

- Joshua Hawley

- Apr 29, 2025

- 2 min read

Week of April 28, 2025

Economic and Market Overview

As we enter the final week of April, markets are increasingly pricing in an accommodative policy shift by the Federal Reserve. Fed Funds futures imply almost 90 basis points of cuts by year-end, with the implied Fed Funds rate expected to decline to 3.44% by December. The probability of a cut as soon as the June FOMC meeting stands at 58.8%, and 64.7% for December, signaling a broad consensus on easing monetary policy.

Interest Rate Movements

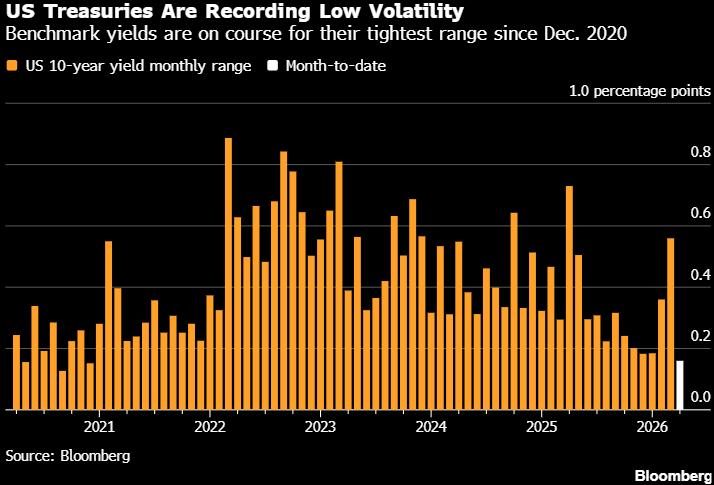

The U.S. 10-year Treasury yield opened the week at 4.26%, slightly firmer than late last week but still well below March levels. Yield curve slopes have steepened modestly, with the 2s/10s spread at 0.50% and the 5s/30s spread at 0.82%, pointing toward reduced recession risk pricing.

Forward Curves and SOFR Trends

Forward curves continue to project significant rate normalization. The 1-month Term SOFR remains stable at 4.32%, but forward estimates suggest a steady decline toward 3.20%-3.25% by mid-2026. Swap spreads have narrowed slightly across tenors, and the 10-year SOFR swap rate stands at 3.76%, suggesting lower long-term borrowing costs ahead.

Agency Debt and CRE Finance Update

In agency debt markets, Fannie Mae 10-year DUS fixed rates for Tier 2 assets are quoted around 5.74%, while Freddie Mac fixed rates are similarly priced near 5.63%. The slight decline in swap rates and treasury yields has compressed agency spreads, offering borrowers improved terms compared to earlier this quarter. Given upcoming economic volatility, this may present an attractive window for refinancing or new loan originations.

Equity and REIT Performance

Major U.S. indices opened the week recovering from prior declines:

S&P 500 is at 5,525,

Dow Jones at 40,114,

Nasdaq at 17,383.

However, market volatility remains elevated, with the VIX volatility index at 25.41, up significantly month-over-month. In REITs, multifamily and healthcare sectors maintain relative stability, though mortgage REITs are offering historically high dividend yields, reflecting continued credit market stress.

Commodities and Currency Outlook

Gold prices have surged to $3,280/oz, up over 7% month-on-month, driven by central bank buying and geopolitical hedging. Crude oil prices declined further to $62.95/barrel, highlighting global demand concerns.The U.S. Dollar has strengthened notably against major currencies, with EUR/USD trading around 1.13 and USD/JPY near 143.45.

Key Economic Data Ahead

This week's economic calendar is critical for near-term market direction:

April 29: JOLTS Job Openings, Consumer Confidence

April 30: GDP QoQ (Advance), PCE Price Index, Personal Income & Spending, Pending Home Sales

May 1: Initial Jobless Claims, ISM Manufacturing PMI

May 2: Nonfarm Payrolls, Unemployment Rate

Particular attention will be on core PCE inflation and employment figures — critical inputs into the Fed’s June rate decision framework.

Comments