IGA Capital Weekly Market Update

- Joshua Hawley

- Apr 8, 2025

- 2 min read

April 7, 2025

Source: Bloomberg, Walker & Dunlop, Fannie Mae, Freddie Mac

Macroeconomic Overview

Global markets began Q2 2025 with a cautiously optimistic tone. While inflation data is anticipated later this week, current market pricing reflects moderate disinflation, a weakening dollar, and easing long-term treasury yields—setting the stage for a recalibration of forward risk appetite in both public and private credit markets.

Bond Markets & Treasury Forecasts

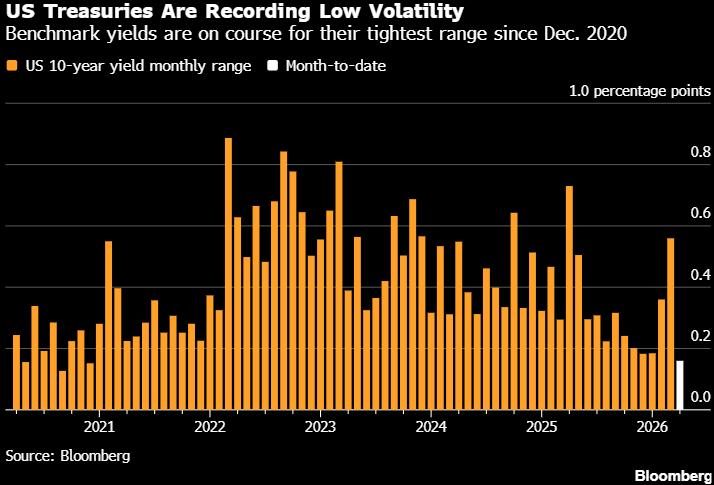

U.S. 10-Year Treasury yields continue to compress. As of this week:

10Y Yield: 4.05% (↓ 15bps from last week)

5Y Yield: 3.72% (↓ 21bps)

Swap spreads also tightened across the curve.

Bloomberg's latest analyst consensus shows 10-year Treasury yields trending lower into 2026, reflecting softening inflation expectations and rate cut assumptions by the Fed.

Source: Bloomberg / Walker & Dunlop Forecast Survey

Agency Loan Pricing – Fannie Mae & Freddie Mac

Despite rate volatility, agency spreads remain firm:

Fannie Mae DUS (Fixed Rate, Tier 2 Pricing):

Term | Gross Rate |

5-Year | 5.42% |

7-Year | 5.41% |

10-Year | 5.47% |

15-Year | 5.75% |

Freddie Mac pricing remains comparable, with 10-year loans quoting between 5.35% and 5.55% across underwriting tiers.

Equity Markets & REIT Performance

REIT valuations continue to face downward pressure. Equity Residential (EQR) and AvalonBay (AVB) both hovered near 52-week lows, while Residential Mortgage REITs like AGNC and TWO now yield upwards of 16%, reflecting heightened credit spread risk in mortgage portfolios.

REIT | Price | Dividend Yield |

AGNC | $8.60 | 16.75% |

NLY | $18.13 | 14.62% |

CIM | $11.01 | 13.26% |

Multifamily REITs remain relatively more stable, averaging 3.7% – 4.5% dividend yields.

FX & Commodities

Gold: $3,009/oz (↓3.2% WoW)

Oil (WTI): $60.09 (↓13.9% WoW)

EUR/USD: 1.09 (↑1.2%)

USD/JPY: 146.82 (↓1.8%)

The U.S. dollar weakened moderately, supporting EM capital inflows and alternative asset pricing.

Upcoming Key Data Releases

Date | Event |

April 8 | NFIB Small Business Optimism |

April 10 | CPI / Core CPI |

April 11 | PPI / University of Michigan Sentiment |

IGA Capital Perspective

With yields trending downward and macro data cooling, borrowers and sponsors should begin preparing to re-enter markets before spreads tighten further. Our current pipeline includes:

Renewables,

Fixed Income Opportunities,

Strategic Mineral Projects,

Pre-IPO,

Real Estate.

For a tailored range-of-terms proposal, please reach out directly or visit: iga.capital/news-updates

Comments