IGA Capital Weekly Market Update

- Joshua Hawley

- Mar 17

- 4 min read

Happy St. Patrick's Day from IGA Capital,

Tuesday, March 17, 2026

Global markets remain in a state of high-velocity turmoil as the conflict with Iran enters its third week. The S&P 500 has retraced to November lows, with the VIX approaching the 30-handle—a clear indicator of systemic fragility. At IGA Capital, we identify Brent Crude at $100/bbl as the primary lynchpin destabilizing traditional portfolios. The 65% surge in energy costs over the last fortnight has invalidated backward-looking inflation data (CPI/PCE), rendering traditional macro signals secondary to real-time geopolitical developments.

Breakdown of Traditional Hedges

The Treasury Trap: US Treasuries have failed to provide the "Safe Haven" bid expected in wartime. Deficit fears and a rekindled inflation narrative have pushed 10-year yields toward 4.30%, as the market effectively dismisses pre-war economic prints as legacy artifacts.

Currency & Gold Dynamics: The US Dollar has advanced 2.6% on a weighted basis, bolstered by its net energy exporter status. Conversely, Gold has found a floor near $5,000/oz, though it has yet to embark on a sustained rally, suggesting a market that is currently "cash-preferential."

Monetary Pivot: Market odds for a Federal Reserve rate cut have been aggressively pushed back to December 2026, as the "War Premium" creates a stag-flationary shadow over global growth.

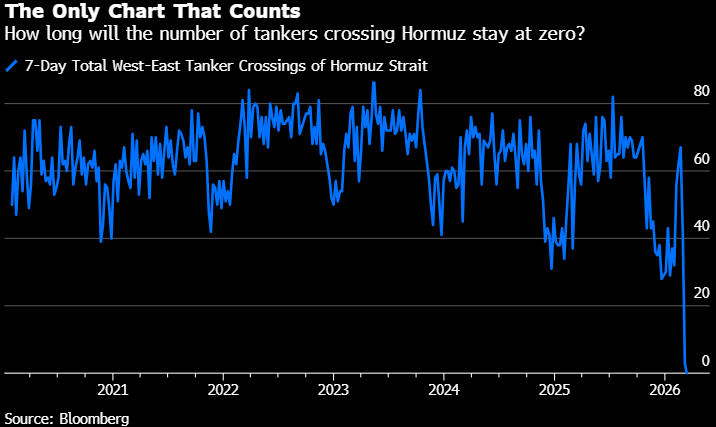

Geostrategy & Supply Chain Disruption

The closure of the Strait of Hormuz—the world’s most critical energy artery—has brought shipping to a near standstill. Beyond oil, the "Vicious Spike" in fertilizer and jet fuel prices poses a direct threat to global food security and logistics. While G-7 strategic reserve deployments offer a temporary psychological buffer, the historical precedent is sobering: Oil shocks in 1974, 1981, 1990, 2001, and 2008 all preceded US recessions.

IGA Strategic Outlook: Positioning for the "Violent Reversal"

While equity sell-offs currently reflect positioning shifts rather than a total erosion of fundamentals, the sustained pressure on corporate profit margins is real. At IGA Capital, we are advising our partners on three core fronts:

Private Credit Resilience: Navigating the rising "angst" in private lending markets by shifting toward asset-backed, short-duration structures.

Infrastructure Sovereignty: Prioritizing investments in "Friend-Shoring" trade corridors that bypass current chokepoints.

Structured Energy Finance: Utilizing structured trade instruments to manage the extreme volatility in the energy and soft-commodity sectors.

Institutional Insight:

"Markets are currently toggling between 'Short-Term Disruption' and 'Prolonged Conflict.' This environment demands a transition from passive asset allocation to Active Capital Guardianship. We remain positioned for a violent market reversal the moment a credible diplomatic off-ramp emerges, but until then, liquidity and collateral control are the only true hedges."

Strategic Market Intelligence: The Geopolitics of Inflation and Bond Volatility

The "Safety" Mirage The global $31 trillion sovereign debt market has entered a period of profound restructuring as geopolitical volatility in the Middle East—specifically the intensification of the Iran conflict—redefines the "Safe Haven" narrative. For the second consecutive week, Treasuries have faced aggressive liquidation, with the asset class failing to act as a reliable hedge against equity drawdowns.

Technical Analysis: Yield Surges & The "MOVE" Spike

Benchmark Yields: The 10-year Treasury yield has aggressively retested the 4.27%–4.29% corridor, surging nearly 30bps since the conflict's onset. Concurrently, the 2-year yield has breached 3.70%, effectively challenging the Federal Reserve’s interest rate on reserve balances for the first time in over three years.

Volatility Gauges: The speed of this yield recalibration has catapulted the MOVE Index to nine-month highs (peaking near 95.30), a stark reversal from the multi-year lows witnessed in January.

Data Irrelevance: Investors are currently dismissing backward-looking macro indicators (CPI/PCE). Despite data meeting cooling expectations, the market remains focused on the forward-looking "War Premium," betting that central banks must maintain a hawkish posture to combat supply-side shocks.

IGA Strategic Outlook: The Oil-Inflation Nexus We anticipate that Treasury yields will continue to track geopolitical headlines with high sensitivity. The critical pivot point lies in the duration of the conflict: at an estimated cost of $1 billion per day, the fiscal weight on the U.S. outlook is substantial.

Interbank and European Rates

Secured Overnight Financing Rate (SOFR): The 1-Month Term SOFR is currently 3.68%, and the 30-day Average SOFR is 3.65%.

EIBOR: As of March 13, 2026, the 3 Months Emirates Interbank Offered Rate (EIBOR) stands at 3.563360%.

ECB Key Interest Rates: The European Central Bank's key rates, as of the last available change on March 12, 2025, are:

Main refinancing operations rate: 2.65%

Deposit facility rate: 2.50%

Marginal lending facility rate: 2.90%

Commodities Pricing

Commodities markets continue to be volatile, primarily due to the war's impact on energy supply.

Oil: Oil prices (using the general pricing benchmark) were at $97.15 as of March 16, representing a 54.7% change over the last month. Brent settling around $100/bbl for the first time since 2022.

Gold: Gold is finding support near the $5,000/oz level, with a reported price of $4,997.03 (up 1.6% 1 Month).

Silver: Silver pricing as of March 16 was $78.93, up 4.8% over the last month.

Impact on Asian Economies: Japan and South Korea

The escalating tensions in the Middle East are generating significant market shocks in energy-import-dependent Asian economies, raising concerns about stagflation.

Japan

Market Reaction: The TOPIX has declined by more than 4% over the past two trading days, and the Japanese Yen (JPY) has depreciated nearly 1% against the USD, contrary to its traditional safe-haven status.

Economic Data: Japan's 10-year government bond yield is 2.24%, with annual Consumer Price Index (CPI) at 1.50% and Gross Domestic Product (GDP) growth at 1.00% (YoY). Unemployment is 2.70% (YoY).

Policy Outlook: The Bank of Japan is likely to be more cautious on policy normalization, potentially delaying its next rate hike.

South Korea

Market Reaction: South Korea has experienced a "triple weakness," where stocks, bonds, and the won are all falling. The KOSPI has declined by more than 7% over the past two trading days, and the Korean Won (KRW) has been the worst-performing currency in Asia, weakening by more than 2% against the USD.

Bond Yields: The 10-year government bond yield has risen to 3.68% as of March 16, amid renewed inflation pressures from rising oil prices.

Policy Outlook: The Bank of Korea faces a trade-off between controlling inflation and supporting growth, and may opt to extend its policy rate hold into the second half of the year.

Regards,

Joshua

Comments