IGA Capital Macro Markets Update

- Joshua Hawley

- Jun 1

- 4 min read

June 1, 2026, Dubai UAE

Executive Summary

Global financial markets closed last week on a highly bullish note. Equities hit record highs, driven by ongoing artificial intelligence (AI) momentum and optimism surrounding a potential 60-day ceasefire extension in the Middle East. This geopolitical shift directly triggered a major pullback in energy markets, leading to a strong rally in fixed income as Treasury yields fell across the curve. While the policy debate within the Federal Reserve remains fractured under newly sworn-in Chair Kevin Warsh, market-implied odds for an additional rate hike by year-end dropped substantially.

Macro & Equities

Equities extended a historic winning streak, with the S&P 500 logging its ninth consecutive weekly advance—a feat achieved only four times since 1985. The index has now rallied nearly 20% from its March lows. Both the Nasdaq 100 and Dow Jones Industrial Average gained over 1%.

AI Dominance: The AI sector remained the primary market engine. Dell surged 33% on exceptional revenue tied to AI server demand, while Micron crossed the $1 trillion market cap threshold for the first time due to intense memory chip demand.

Valuations & Outlook: Goldman Sachs raised its year-end S&P 500 target to 8,000, attributing the adjustment to AI-driven earnings momentum rather than stretched valuations. The broader outlook remains supported by healthy corporate earnings and a resilient jobs market.

The Week Ahead: Market participants are focused on the upcoming May nonfarm payrolls print to gauge the ongoing structural resilience of the labor market.

Commodities & FX

Geopolitical developments in the Middle East dictated price action across the commodities complex, which in turn heavily influenced global risk appetite and currency dynamics.

Commodities

Crude Oil: Energy prices collapsed as markets priced in the potential restoration of shipping flows through the Strait of Hormuz. WTI crude tumbled to $87/bbl. For the month of May, Brent crude fell 19%, marking its worst monthly performance since March 2020.

Geopolitical Volatility: The commodity risk premium remains highly volatile. Despite a tentative 60-day ceasefire extension and nuclear talk framework negotiated by the US and Iran (pending President Trump's sign-off), the situation remains fluid. Iranian state TV reported an unofficial draft MOU granting Iran "exclusive authority" over Strait vessel passage, including navigation fees and entry denials. Conversely, US Defense Secretary Hegseth stated the US blockade remains in place, and the US military subsequently fired a missile into a commercial ship attempting to reach an Iranian port on Saturday evening.

Risk-On Flows: The sharp reduction in the energy-driven inflation premium firmly bid global risk appetite. The breakdown in oil prices acted as a relief valve for major currency pairs tied to global growth, shifting capital out of defensive postures as equity markets marched to record highs.

Interest Rate Differentials: The repricing of fixed income markets—driven by falling yields and lower implied Fed hike expectations—realigned short-term yield differentials, taking some immediate upward pressure off the broader rate complex.

Fixed Income & Treasury Yields

The Treasury market staged its strongest weekly rally since the onset of the Iran conflict four months ago. Yields fell 9–12 bps across the curve from the previous Friday's close, unwinding the inflation premium that had previously pushed yields to multi-year highs.

Key Levels: The 10-year US Treasury yield fell to 4.43%, while the 30-year yield dropped back below the key 5% threshold.

PCE Data Catalyst: April PCE data provided a secondary modest relief signal. Headline PCE accelerated to 3.8% YoY (the highest since May 2023) and core PCE reached 3.3% YoY, with a monthly print of 0.4%. However, because both monthly metrics came in 0.1% shy of consensus expectations, fixed income markets locked in gains heading into the weekend.

Yield Outlook: A sustained yield rally will likely require a finalized Iran deal alongside signs of labor market softening in the upcoming ISM surveys and May nonfarm payrolls report (where economists project an addition of 89k jobs versus April's 115k).

Federal Reserve & Monetary Policy

The policy debate among FOMC officials has sharpened considerably during Kevin Warsh’s first full week as the 17th Federal Reserve Chair. Warsh, who was sworn in on May 23, faces the challenge of managing an environment with elevated headline inflation despite his stated agenda of pursuing lower rates and a smaller balance sheet.

Divided FOMC Commentary: * Hawkish: KC Fed President Schmid noted the Fed is not highly restrictive and may need to tighten further via the balance sheet. St. Louis Fed President Musalem stated the probability of a rate hike is greater than zero, noting the Fed is currently missing on its inflation mandate.

Dovish/Divergent: Philadelphia Fed President Paulson characterized current price pressures as temporary shocks rather than structural inflation. Fed Governor Bowman warned that reacting to temporary energy spikes would introduce unwarranted policy restraint.

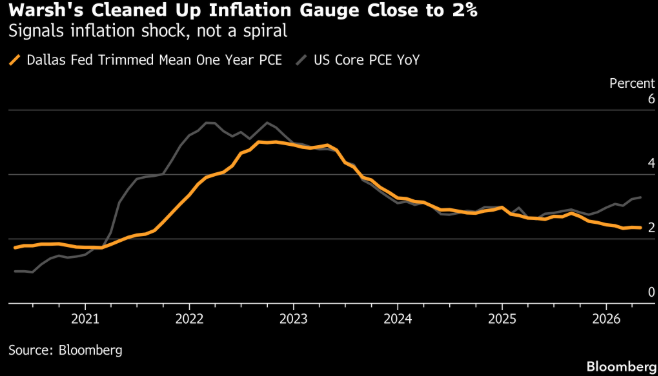

Inflation Metrics: The Dallas Fed Trimmed Mean PCE—reported to be Chair Warsh's preferred inflation gauge—showed 12-month inflation through April at 2.35%, significantly closer to the Fed's 2% target than headline or core figures.

Political & Executive Support: Treasury Secretary Bessent stated he is "100% in favor" of Warsh eliminating forward guidance, declaring that "rates peaked the day before Warsh was sworn in." President Trump also indicated a softening of public pressure, stating he will let Warsh "do what he wants to do" with rates.

Market-Implied Expectations: By week's end, markets priced in a 57% chance of a 25bp hike by year-end, down sharply from 95% the prior week.

FOMC Meeting – Implied Fed Funds Rate

Implied Overnight Rate: 3.629%

June 17, 2026 (Mid-Year Meeting): 3.643%

December 9, 2026 (Last Meeting of 2026): 3.772%

June 9, 2027 (Mid-Year Meeting): 3.862%

Economic Calendar

Date | Indicator / Event |

Monday, 6/1 | S&P Global US Manufacturing PMI; ISM Manufacturing |

Tuesday, 6/2 | JOLTS Job Openings |

Wednesday, 6/3 | ADP Payrolls; S&P Global US Services PMI; ISM Services; Durable Goods; Fed Beige Book |

Thursday, 6/4 | Initial Jobless Claims |

Friday, 6/5 | Nonfarm Payrolls; Unemployment Rate |

Next Week | Trade Balance; Existing Home Sales; CPI; 10-year U.S. Treasury Auction; PPI; University of Michigan Consumer Sentiment |

If you have any questions or would like to discuss a loan request, please reach out to me using the contact information below.

+971 50 764 0788

Comments